FTR Associates president Eric Starks frequently gets questions from people in the industry who don’t completely understand monthly market indicator data.

They ask him, “What are some of the nuances there? What are the things I should be looking at to make better decisions?”

To help them, he gave a presentation, “Using the Monthly Market Indicators.”

The key takeaways:

• Retail sales.

“Why do we care about retail sales? Inventory is clearly part of the equation. If something is produced, does it get put into service? No. Retail sales is a pure demand-driven number. It is actually something getting put into service. That means truckers taking it, activating it, and it actually is in the marketplace. That is a huge reason why we start all forecasts with retail sales. Inventories play into that. It’s a big issue. If the retail sales market is collapsing and production continues to go higher, are you going to continue to produce? Absolutely not.

“When you look at monthly data, there are nuances there. At the end of 2013 and early 2014, retail sales jumped up in December and production fell off. The same thing happens in reverse at the beginning of the year. If you’re in an environment where you’re worried about production, retail sales are not very helpful to you. But for me, understanding the retail market is really important because that up and down has a big impact on putting more equipment into marketplace.”

• Build versus factory shipments.

“Factory shipments and the production line are pretty close. Typically, the way we try to look at it is that it’s a build if it goes down the assembly line. Depending on how systems are set up, it doesn’t necessarily get counted that way. A factory shipment is actually shipped out of a facility. For some, the build and factory shipments are actually are the same.”

• Seasonality in Class 8 market.

“We’re getting to the point where we’re getting into the seasonal market over the next several months. Traditionally, we see seasonally weak orders happen in the May-to-September time frame. When you hit October, November, and December, things start to pick up. You have to understand. We’ve finished the shipping season. Then carriers finally can assess their needs and say, ‘What do I need for next year?’ And then they start placing orders. You need to understand seasonality.

“2014 clearly is about what we’d expect seasonally. This is a good sign for the short term within this market. On a build cycle, it’s a little bit harder to see seasonality, but it’s clearly there. When you get to the holiday season, there is a shutdown time. It’s not a prevalent as it used to be. When we look at it on a quarterly basis, it shows up. Typically the second quarter tends to be the highest-producing quarter of the year. People are saying, ‘I want delivery of my trucks before the freight season kicks in.’ So they’re producing a bunch of trucks to get them out the door.”

• Orders are a leading indicator for production.

“This is telling us there is an upside pressure within the build cycle. So orders are the best indicator of future demand in the short term when you’re looking out three to six months. OEMs over the last several years have been very diligent about keeping their books clean. For now, most everybody’s reporting it within a 12-month window. That helps keeps the books clean. The challenge this creates is that you can’t compare backlogs today to where they used to be. It creates a challenge because there will be some anomalies throughout the year when orders get booked. Let’s say a multi-year order comes in today. They say, ‘I want delivery in October of 2015.’ Well, that order doesn’t get booked in there necessarily. It will get booked in there in October of 2014, 12 months out from when it goes in. That’s the general process. So there are times we see a spike and we go, ‘What happened?’ Well, a multi-year order finally got activated in the system.”

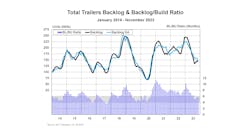

• New truck lead times.

“It’s also backlog-to-build ratio. We are measuring what the backlog today is relative to the size of production. Right now, it’s close to five months backlog-to-build. That means on average it takes five months to get it into the system and get you your truck. Now, that’s not reality but that’s what the average is saying. We use this as a pressure gauge to understand if there is significant pressure in the system to increase production or decrease production. It is a tool. It’s not a perfect guide. For trailers and Class 8 trucks, it’s the same type of analysis. Anytime you get above six months, then you start seeing noticeable pressure on OEMs to increase production. When it gets below four, there is significant pressure in the system to cut production. It’s just a general rule of thumb. This is not the gospel truth. But it’s a helpful guide. Is there significant movement in the manufacturing system? Right now, there is not significant pressure just based on backlog to rapidly increase production levels.”

• Inventory-to-sales ratio.

“What is it telling us? It’s a great gauge to tell us if there is excess inventory or not enough inventory in the system. In North America, this average likes to sit in 1.8 or 1.9 months of inventory on hand. But since the Great Recession, we’ve seen a shift where all of a sudden they are willing to hold more inventory on hand, and it sits between two and two and a half months of inventory. Any time it gets above one and a half, it starts to make me a little bit nervous. It says there is pressure in the system to edge back production levels or you have to see a noticeable increase in the sales environment. Usually, it’s the first one. In ’09, we saw the number spike, and when it does, you’d better know the brakes are going to be hit on production.”

• Cancellations.

“Are they telling us anything about the current market? They are a useful tool to ascertain, ‘Are people getting nervous about the current environment?’ We have found that, yes, there was a pretty decent spike in numbers back in July for cancellations. But when you look at it as a percentage of backlog, it’s a small number. So I don’t see a trend here. We’re looking for noticeable changes or trend changes.” ♦