The U.S. trailer industry provided a second consecutive "upside surprise" in April 2026, as net orders increased despite historical patterns that typically favor a spring slowdown. Data from FTR and ACT Research suggest that while the market remains in a challenging environment, it is moving toward stabilization and modest improvement.

April by the Numbers: According to FTR, U.S. trailer net orders rose to 19,953 units, an 11% increase month-over-month. This figure significantly outpaced the 10-year April average of 15,474 units and represented a 100% surge compared to April 2025. ACT Research reported a similar preliminary figure of 19,400 units, noting a 3% sequential increase from March. When seasonally adjusted (SA), ACT placed the order rate at a robust 26,800 units, a 43% jump from the March SA rate.

“April trailer demand was better than expected, but a durable upcycle will likely require stronger fleet margins, higher trailer utilization, further absorption of excess capacity, and clearer visibility into trade-related costs,” said Dan Moyer, FTR senior analyst, commercial vehicles.

This year-over-year growth, which ACT measured at nearly 127%, is largely attributed to a comparison against the "tepid" and "subdued" intake seen in April 2025. Jennifer McNealy, director of CV market research at ACT Research, noted that the traditional annual order cycle appears to have shifted, with upticks that typically begin in the fall being delayed until December.

Production discipline, backlog resilience

While demand strengthened, trailer manufacturers maintained a high degree of production discipline. FTR reported that April builds were essentially flat month-over-month at 17,576 units.

Because net orders outpaced production—a trend ACT has observed in three of the first four months of 2026—backlogs began to grow. ACT noted a 3% month-to-month increase in backlogs.

“However, this was not enough to pump much lifeblood into the anemic backlogs,” McNealy said. “YTD, backlogs contracted more than 13% compared to the first trimester of 2025.”

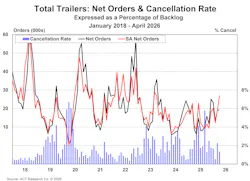

The industry also saw an improvement in the stability of these orders. The cancellation rate as a percentage of the backlog dropped to 1.4%, down from 2.3% in March. Despite this improvement, cancellations remained "elevated" and broad-based across most trailer segments, according to ACT Research.

Stabilization vs. policy risk

Industry analysts remain cautiously optimistic but emphasize that the current rebound is not yet a broad expansion. Moyer suggested that the market is moving from "deterioration toward stabilization," driven primarily by replacement demand and selective activity from stronger fleets rather than a major capacity increase.

Several "overhangs" continue to weigh on the sector’s long-term outlook, per FTR:

- The power-unit disconnect: Fleets are currently prioritizing investments in Class 8 tractors over trailers, a trend that may continue to cause trailers to lag behind trucks in the near term.

- Regulatory and policy risks: Changes in Section 232 steel and aluminum tariffs, alongside antidumping and countervailing duties investigations into van trailers, are creating pricing and sourcing volatility.

- Economic pressures: High petroleum prices and uncertainty in key freight-generating sectors continue to influence the purchasing decisions of fleet managers.

Both firms agree that a durable upcycle will require clearer visibility into trade-related costs and higher trailer utilization rates. As the industry enters the final two months of the second quarter, all eyes will be on whether this momentum can be sustained or if traditional Q2 weakness will prevail.

About the Author

Kevin Jones

Editor

Kevin has served as editor-in-chief of Trailer/Body Builders magazine since 2017—just the third editor in the magazine’s 60 years. He is also editorial director for Endeavor Business Media’s Commercial Vehicle group, which includes FleetOwner, Bulk Transporter, Refrigerated Transporter, American Trucker, and Fleet Maintenance magazines and websites.

Working from Beaufort, S.C., Kevin has covered trucking and manufacturing for nearly 20 years. His writing and commentary about the trucking industry and, previously, business and government, has been recognized with numerous state, regional, and national journalism awards.