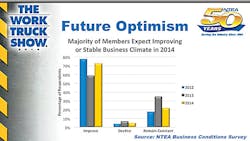

2014-2015 projected to be better than 2013, with majority of NTEA members expecting improving or stable business climate

In his “State of the Industry” presentation, NTEA executive director Steve Carey listed these pros:

• The US dollar remains relatively weak.

• There is room for growth as consumers and businesses have available cash.

• The average age of trucks is still high.

• Low inflation.

• Low interest rates.

• The construction industry is growing.

Carey listed these cons:

• Labor market imbalance.

• Consumer confidence is still a bit shaky.

• Slow growth in EuroZone and the BRICS (Brazil, Russia, India, China, and South Africa).

• Political uncertainty domestically and internationally.

Carey said most of the findings from the NTEA Business Conditions Survey exude optimism. For example, since the beginning of 2013, 51% of the member firms have increased employees, 42% have held constant, and only 7% now have fewer employees.

At end of 2013, 58% reported higher sales velocity than in the middle of the year. Last year’s result for 2012 versus 2011 results: 74% reported higher velocity than in 2011, 13% were unchanged from 2011, and 13% were lower.

The majority of members expect improving or stable business climate in 2014, with 73% expecting an improvement (up from 60% a year ago), 5% expecting a decline (down from 8%), and 22% expecting it to remain constant (down from 32%).

In plant utilization, 15% are at full capacity (up from 10%), 56% are at three-quarters to full (up from 53%), 26% are at half to three-quarters (down from 35%), and 3% are at half or less (up from 2%).

Thirty-seven percent had higher backlogs than at the middle of 2013. Last year, NTEA compared the beginning of 2012 versus year-end. During that time, 43% said backlogs were higher, 39% unchanged, and 18% lower.

In lead times, 29% had 60 days or more (down from 32% a year ago), 29% had 30-60 days (down from 31%), and 42% had 30 days or less (up from 37%).

Asked about current business challenges, 68% listed overall economic conditions (down from 84% last year), 50% listed government financial or regulatory policy (up from 45%), 39% listed continuation of a poor housing market (up from 22%), and 22% listed low consumer confidence (down from 28%).

Employees remain a concern

In areas of concern, 57% listed finding and keeping qualified employees (up from 76%) and 32% listed complying with regulations (up from 39%).

The 2014 Fleet Purchasing Outlook Preview tried to measure purchasing intent. Asked if their fleet plans to acquire trucks this year, 91% said yes, an increase of 5%, and 33% said they will acquire more this year than last year, a 7% increase.

On the topic of fleet age, 46% said it will increase, 33% said it will stay the same and 21% said it will decrease—identical to last year.

Asked if truck acquisitions in the coming year will be funded, 11% said funding is questionable (down from 12%) and 33% said funding is likely (up from 31%).

In the Channel Relationship and Market Trend Report, a majority of distributors are maintaining or growing their dependence on manufacturers.

On the topic of change in distributor involvement with manufacturers, 36% increased, 15% decreased, and 49% stayed the same

“It is clear from the data that relations between distributors and manufacturers are important, given that 85% of respondents declare their dependence is increasing or staying the same,” Carey said. “Furthermore, these strengthened relationships may be correlated to their increases in sales volume.

“Company size proves to be a relevant factor in how distributors are positioning themselves and applying competitive tactics. There were clear differences in survey responses for distributors with annual sales less than $5 million, between $5-10 million, and greater than $10 million.”

Over the last five years, manufacturers have made some adjustments to their sales philosophy in order to address changing economic and market conditions.

Over the past year, 26% of manufacturers increased their reliance on distributors, 25% increased reliance on direct selling, and 49% stayed the same. ♦

About the Author

Rick Weber

Associate Editor

Rick Weber has been an associate editor for Trailer/Body Builders since February 2000. A national award-winning sportswriter, he covered the Miami Dolphins for the Fort Myers News-Press following service with publications in California and Australia. He is a graduate of Penn State University.