Trailer orders unseasonably solid: reports

U.S. trailer demand was “resilient” in May, increasing 1% month over month to 20,189 units, which represented a surge of 249% year over year versus a very weak level in May 2025, FTR reported.

And those orders were far above the 10-year May average of 11,649 units, indicating better-than-seasonal momentum into late spring. Dry van trailers led the strength, but other key trailer types were strong as well, and almost all logged improved orders from a year earlier.

“Despite the stronger May order intake, the market still does not appear to be entering a broad-based upcycle, especially with seasonally slower order months approaching,” said Dan Moyer, FTR senior analyst, commercial vehicles. “Rather than widespread capacity expansion, demand remains concentrated in replacement activity, fleet-specific needs, and dry van normalization with support from solid flatbed demand.

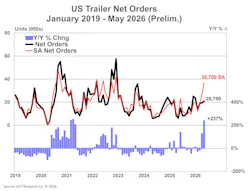

ACT Research reported similar preliminary numbers for May, at 20,700 units. Seasonal adjustment (SA) at this point in the annual order cycle takes the month’s volume to 36,700 units. Final ACT Research trailer industry data for May will be available later this month.

“A sequential drop in net orders is typically expected, as May traditionally marks the second weakest order month of the annual order cycle,” said Jennifer McNealy, director, CV market research and publications at ACT Research. “That said, this year’s cycle initially looked like it had been delayed a few months, as the order upticks that should have started in September or October of last year didn’t actually begin until December, but now may be buttressed by the rising freight rates. Regardless of the timing, the order upticks certainly are welcome, but caution remains a strategy for some trailer purchasers.”

Given accelerating freight rates and rising carrier confidence, ACT Research has raised the question for the last two months about whether more surprisingly high order intake months were still coming, or whether traditional Q2 order weakness would prevail as fleet decision-makers continue to hesitate about placing trailer orders while accelerating Class 8 tractor purchases instead in 2026, she noted.

“Based on the May data, we now know there was at least one more month of improved order intake in the pipeline, but it remains to be seen how the final month of Q2, as well as how Q3, will unfold,” McNealy said.

Build remains muted

Indeed, U.S. trailer builds declined 6% month over month in May to 16,553 units and were down 1% y/y, showing that trailer manufacturers remain cautious despite improved orders. Production for the year to date was essentially flat compared to 2025 at 79,482 units as net orders continued to outpace build, FTR reported.

“Cost pressures are building and are reflected in May’s sharp increase in the already-elevated Producer Price Index for truck trailers and chassis,” FTR’s Moyer said. “A recent change in how Section 232 tariffs are applied means higher overall tariffs on trailers, and upcoming antidumping/countervailing duty exposure for van-type trailers and subassemblies could add more costs on top of Section 232 tariffs.

“This situation may create opportunities for domestic manufacturers and suppliers, but those opportunities also could tighten build slots, extend lead times, and strain the supply of components or labor. The result could be firmer domestic pricing and less consistent order flow even without a broad increase in underlying trailer demand.”