TRAILER production is expected to peak this year at 265,000 units, then decline to 254,000 in 2015 and 230,000 in 2016.

When FTR Associates president Eric Starks presents those numbers, he invariably gets questioned: “Gosh, why do you have things slowing down to 230,000?”

His answer is quite simple, and it’s as much of a question as it is an answer.

“Well, is 230,000 really and truly a slowdown?” he said. “It’s a very healthy number for this market. At 230,000, you’re still above replacement demand.

“So let’s look at this from a fleet perspective. The overall fleet wants to grow. How much freight do they have in the system and how does the overall fleet need to be? The fleet is going to continue to grow, but at a slower pace—more in line with the freight environment.”

Since the second quarter of 2011, quarterly trailer production has been at least 53,000. But it jumped dramatically to 69,000 in the second quarter of this year, moved up to 73,000 in the third quarter and is projected to be 66,000 in the fourth quarter.

“All of a sudden, the dynamics have changed,” Starks said. “We’re sitting in the high 60,000, low 70,000 range. Over the next year or year and a half, we’re expecting 60,000 to 70,000 units on a quarterly basis. From a risk perspective, the greatest risk is in second half of 2015.”

In terms of total trailers in the US, backlogs were up 56% year-over-year in August.

“That’s a huge environment,” he said. “It suggests production is higher and they can support that, because the backlogs are there.”

Equipment demand by type:

• Dry van. “Strong orders and a healthy backlog will sustain build levels. We don’t see a whole lot of upside pressure, but it will stay at healthy levels.”

• Reefer van. “There is upside pressure on build rates due to large backlogs.”

• Flatbed. “Limited backlogs will keep production in check for the short term. One of the growth areas is in flatbeds on the freight side. We’re seeing strong growth in the flatbed market, but order activity has started to ease. Some of that is you have already have a lot of stuff in the pipeline.”

• Tanks. “Recent acceleration in tank orders will likely push production demand higher. We’re seeing orders outpacing production, and that suggests upside pressure in that market.”

He summarized the following areas:

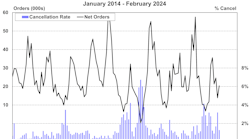

- Trailer build activity. “From 2011, build numbers went up and then just stopped. But all of a sudden, something changed in the last few months, and build numbers have jumped up. Production has moved higher. That is not a bad thing but means we have to recalibrate ourselves to start thinking differently.”

- Trailer net order activity. “We typically see strong orders from December to February. Those sustain us for the balance of the year. You see seasonal falloff in the summer. What’s different this time is you still saw seasonal falloff but levels stayed up significantly higher than we’d normally expect. August numbers are up 45%, and that’s a decent number. That puts pressure on the system.”

- New trailer lead lime (backlog-to-build ratio). “Any time you’re between four and six months, it suggests you’re in an environment where you don’t have to increase or reduce production levels. Now we’re sitting near five months of backlog. It suggests we’re fairly right-sized within the market. The need to pull back or increase production isn’t there. We think production levels are going to be sustained for the near term at these higher levels.”

- Total trailer capacity utilization. “Right now, it’s 95%, which is a pretty high number in the market. Some of the pressure of why orders are coming in is because capacity is tight out there. This is a good thing. Our model suggests a fairly tight market for the next year to year and a half.”

Starks said trailer dealers need to understand that the media depiction of the economy—“that it’s blah and isn’t doing much of anything,” in his words—isn’t supported by the statistics in the different sectors of the economy.

“We need to get on the same page,” he said. “Why does everybody buy a trailer? To move freight. This is huge. If you do not have freight to move, you do not buy a trailer. Period. We have to get that in perspective. Most of the freight that gets moved is in manufacturing. It’s not the sexy retail stuff.”

The ISM Manufacturing Index has been expanding since the end of 2012.

“By and large, it’s looking pretty good,” he said. “Manufacturing is doing well. This is why the equipment market is doing fairly well.”

Payroll employment peaked at 304,000 in April, dropped to 229,000 in May, went back up to 267,000 in June, then fell to 212,000 in July and 242,000 in August.

“When you’re looking at numbers in the economy, you want to see around 200,000 to 300,000 per month,” he said. “But when I go and talk in industry sessions, people are struggling to hire quality people for their workforce. We’re seeing it within the driver environment and we’re seeing it in maintenance. So when we see numbers like this, it makes me scratch my head. You’re not seeing significant growth in the employment numbers, but at the same time people are struggling to find high-quality workers. So it’s a conundrum. We want to see this number go higher. We want to see job growth continuing to happen and continue to see the economy grow.”

He said business activity is near its pre-recession peak. Orders are a great indicator of future activity, and in 2012, people stopped ordering. Since then, there has been strong order activity.

“We’re finally above that peak level we saw in 2008,” he said. “That is a really, really good sign, because if this economy continues to keep moving, we need to see business participating. This suggests in the short term, businesses will continue to buy.

“You have to have inventory, but you hate to have it because you have cash sitting there doing nothing. It’s cash in a different form. We found that in the 1990s, the number came down significantly, from 1.56 months of inventory in 1992 to 1.39 in January 2000. A lot of that was the just-in-time inventory cycle. Then we hit this bottom. It’s been coming up a little, from 1.26 in January 2012 to 1.31 in January 2014.

“There is a different dynamic. People are trying to figure out, ‘What do I do with inventory?’ One of the issues is transportation. It’s very tight, so you can’t have too little inventory sitting on the ground because you don’t have enough in the system. But we don’t want to see the big spike we saw in 2008 and 2009, when it went up to 1.49. Right now, it’s in a nice range. There is a lot of pressure in the system from the inventory perspective.”

There were 2.3 million housing starts in 2006, and then the bottom fell out and they dropped to 500,000 in 2009. They have climbed steadily since then, to 960,000 in August.

“Housing is great,” he said. This market has significant upside potential. We would expect to get in 1.4 to 1.5 million, and we’re sitting below one million. I’m looking for opportunities for growth, and housing is one area where we can see that.”

Existing home sales peaked at 4.75 million in July 2013, then plunged to 4.04 million in March of this year. But they were back up to 4.46 million in August.

“When you buy an existing home, you buy carpet, furniture, appliances,” he said. “We started seeing a lot of freight. That started bottoming out and then coming back, and it’s hitting decent levels. We’re in an environment where this is starting to generate additional growth. There’s a little bit of upside pressure.”

The automotive market took a deep dive, with 9.02 million in auto and light truck sales in February 2009, but steady climb took sales to 17.5 million in August of this year.

“Overall, we’ve seen great growth,” he said. “If I had been talking to you a couple years ago and somebody said we’d see over 17 million in auto sales, I’d have laughed. I’d have said no way we’d see that in this cycle. The high 16,000 range is pretty darned good. Is there a lot of growth opportunity here? No. The likelihood we see significant growth in this market is constrained.”

Diesel prices have been reasonable, with the average price of a gallon falling to $3.80 in August.

“Your ultimate customers, the carriers, love fuel,” he said. “It’s a love-hate relationship. They have to pay for it and consume it, but they hate to pay for it. Does this change their cost dynamic? For them, they have fuel surcharges. They can go out to shippers and say, ‘My fuel prices went up. I want to recoup it.’ But it takes time. So we don’t like to see the volatility we see with fuel prices.”

Starks said US freight levels are healthy, with growth in the 4% to 4.5% range. He expects 3% to 4% growth over “the foreseeable future.”

Freight loadings are climbing, but are not expected to reach the 2006 peak until 2016.

“So the question is, ‘Why are people buying all these trailers if we won’t get back to the peak levels we saw in 2006?’ ” he said. “Some of it has to do with replacement cycles and a productivity drop. When you see a drop in productivity, you need more equipment. When productivity goes up, you need less equipment. In the near term, we’re going to see productivity going down, so the need for more equipment becomes greater.”

By segment, he said the flatbed market has the greatest potential and highest growth he expects to see in the freight loadings market.

“Remember the housing numbers? They’re pretty anemic, and we think there’s upside opportunities,” he said. “What does a flatbed haul? Lumber and metal. Those are construction-related items. What’s most concerning is the growth in the dry van market is diluted. We only see 1% to 2% growth as we go into 2016. The dry van market is a large segment out there.”

The Trucking Conditions Index, after hitting 9.8 in August, is projected to hover around 8 for the next year.

“Any time the number is above zero, it suggests that the trucking environment is healthy,” he said. “The further away from zero, the better it is. By the time you get a reading of 10, you’re at critical levels and trucking would have the complete upper hand. That means they can dictate rates, dictate capacity, and can go out and buy equipment. It’s still an environment that’s very healthy for truckers.”

On the downside, regulatory issues—especially Hours of Service—are having a negative impact.

“It’s very difficult for them to get drivers,” he said. “At the end of 2016, we’re going to need 160,000 more drivers just because of regulations. It will either disqualify a driver so he’s no longer able to participate in the workforce or productivity goes down. This is a huge issue. ♦